For aspiring motorists across the United Kingdom, acquiring a driving licence represents an unparalleled milestone of personal freedom. However, the economic reality of entering the motoring landscape is remarkably steep. In 2026, when you aggregate the price of professional driving lessons, theory test bookings, practical examination fees, and the procurement of a first vehicle, the aggregate financial burden can easily exceed thousands of pounds. Yet, the most formidable financial hurdle that stands between a provisional licence holder and the open road is navigating the complex, highly regulated world of car insurance for learner drivers.

Under the statutory framework of the UK Road Traffic Act, every single individual who operates a mechanically propelled vehicle on a public highway must be protected by a valid insurance policy. This mandate applies just as strictly to an individual holding a green provisional licence as it does to a seasoned driver with decades of experience. While professional driving school vehicles are inherently covered by specialist fleet insurance, engaging in private driving practice outside of those paid hours demands independent insurance provisions. Whether your goal is to log extra practice hours in a parent’s family hatchback, master reverse parking maneuvers in a friend’s car, or establish an insurance record within a vehicle you personally own, selecting the correct policy structure is non-negotiable.

Failing to secure exact legal coverage carries life-altering consequences for young or new drivers. The legal and financial penalties for driving uninsured on a provisional licence can permanently derail your motoring ambitions before your practical test date is even confirmed. This exhaustive guide provides an authoritative analysis of the learner driver insurance sector, detailing structural variations, strict supervision rules, accident procedures, and data-backed methods to drive down premium costs.

The Legal Framework: Penalties for Uninsured Private Practice

A persistent and dangerous myth continues to circulate through online forums and student communities: the assumption that a valid provisional driving licence functions as an automatic, temporary pass that grants third-party cover under a parent or relative’s primary car insurance policy. This assumption is completely false. Unless a provisional licence holder’s name is explicitly printed on the certificate of motor insurance for that specific vehicle, or covered via a dedicated standalone learner policy, they are operating the vehicle illegally.

The UK legal system treats uninsured learner driving with zero leniency. If you are stopped by the police while undertaking private practice without appropriate insurance, you will face an immediate fixed penalty fine of £300 and a mandatory 6 penalty points applied directly to your driving record. For an individual who has not yet passed their test, these points remain active and carry over to your full licence.

Crucially, this triggers the catastrophic mechanics of the New Drivers Act. Under this legislation, if a motorist accumulates 6 or more penalty points within the first two years of passing their driving test, their full driving licence is automatically revoked. Consequently, receiving 6 points while still on a provisional licence means that the exact second you pass your practical driving test, your newly obtained full licence is instantaneously cancelled. You will be forced to reapply for a provisional licence, pay for new theory and practical exams, and face significantly inflated insurance quotes due to your conviction record.

The penalties extend beyond the learner. Police officers possess the statutory power to immediately seize, impound, and even crush an uninsured vehicle at the roadside. Furthermore, the individual who permitted you to drive the car—whether a parent, partner, or sibling—can be prosecuted for the specific criminal offence of “permitting the use of an uninsured vehicle.” This secondary prosecution results in separate fines and penalty points on their own driving record, turning an innocent practice session into a multi-car legal disaster.

Comparing the Two Pathways: Named Driver vs. Standalone Learner Cover

When structuring your provisional driver insurance infrastructure, you must choose between two distinct operational pathways. The strategy you select dictates not only your upfront premium expenditure but also the structural distribution of financial risk across your household.

Path A: Adding a Learner as a Named Driver on an Annual Policy

This method involves the primary vehicle owner contacting their current insurance underwriter to formally add the provisional licence holder to their existing annual car insurance policy as an additional named driver. The insurer updates the policy profile, integrates the risk metrics of an inexperienced driver, and issues a Mid-Term Adjustment (MTA) invoice.

- The Core Mechanism: The learner shares the exact same policy shell as the primary driver, granting them identical coverage status (typically Fully Comprehensive) whenever they occupy the driver’s seat.

- The Severe Financial Downside: The overarching vulnerability of this method centers on asset protection. If the learner driver is involved in a collision, scrapes an expensive alloy wheel, or clips a third-party vehicle, the claim must be filed directly against the owner’s primary policy. This action completely compromises the primary policyholder’s accumulated No Claims Bonus (NCB). Furthermore, the primary owner must declare that at-fault accident during every subsequent insurance renewal for the next five years, driving up their household motoring costs significantly. Insurers also routinely charge steep administrative processing fees for both adding a learner and subsequently removing them once they pass their exam.

Path B: Independent, Standalone Learner Driver Insurance

The modern alternative is to procure a specialist, independent provisional insurance policy that sits directly alongside the car’s primary cover without displacing it. This creates an isolated legal contract between the learner and the specialist underwriting provider.

- The Core Mechanism: This standalone policy provides dedicated, comprehensive protection exclusively to the learner driver while they are operating that specific vehicle under appropriate supervision.

- The Asset Protection Benefit: Because this policy functions as a separate legal entity, if an accident occurs during private practice, the claim is processed entirely through the learner’s independent policy. The vehicle owner’s primary annual car insurance policy and their No Claims Discount remain completely insulated and untouched. This isolation provides peace of mind to parents or relatives who are willing to lend their vehicles but cannot afford to jeopardize an irreplaceable 10-year No Claims Bonus. Furthermore, these policies offer granular temporal flexibility, allowing users to buy cover in blocks of 1 hour, 1 day, 1 week, or up to 5-plus months to perfectly match their test preparation timeline.

Direct Comparison Matrix: Financial Risk and Policy Scope

The structural grid below highlights the mechanical differences that web operators and consumers must evaluate when analyzing these two insurance products.

| Operational Dimension | Named Driver Addition (Annual) | Standalone Learner Policy (Temporary) |

|---|---|---|

| Legal Contract Shell | Modifies the vehicle owner’s core annual policy document. | An independent, secondary policy running parallel to the main cover. |

| Primary No Claims Bonus Risk | Extreme Risk. Accidents instantly degrade or reset the owner’s NCB status. | Zero Risk. Claims are isolated; the primary owner’s NCB is fully protected. |

| Mid-Term Adjustment (MTA) Fees | Subject to insurer admin fees for both installation and removal. | No admin fees; policy automatically expires at the end of the chosen term. |

| Temporal Granularity | Inflexible; remains bound to the remaining lifecycle of the annual policy. | Hyper-flexible; configurable from 1 hour up to several months. |

| Long-Term Premium Impact | Accidents increase the primary owner’s renewal rates for 5 years. | Accidents are logged against the learner, preserving the owner’s record. |

| Status Post-Practical Test | Can occasionally transition to a full licence named driver (fees apply). | Voided instantly. Legally impossible to drive home post-examination. |

How Much Does Learner Driver Insurance Cost?

The cost of provisional insurance varies based on standard underwriting factors, including your postcode, age, and the specific car you intend to drive. However, because statistics show that learners under proper supervision actually have fewer accidents than newly qualified drivers, temporary provisional insurance is often surprisingly affordable.

In the current motor insurance market, short-term provisional premiums scale predictably across specific temporal blocks:

- Single-Day Cover (24 Hours): Typically spans £15 to £25, making it highly efficient for focused, single-day intensive parking or junction practice sessions.

- Seven-Day Cover (1 Week): Averages between £35 and £50, ideal for utilizing school holidays or the week preceding a scheduled practical test.

- Twenty-Eight Day Cover (1 Month): Ranges from £85 to £130, providing a sustained window to complement professional lessons.

For context, trying to add a 17-year-old male driver directly onto a parent’s premium as a full named driver on a high-performance vehicle can add thousands to an annual bill. If you are looking ahead to future costs once you qualify, you can review our historical market tracking data regarding the average car insurance cost for a young driver in the UK to understand how premiums adjust across different regions and age cohorts.

Check Out Car Insurance Estimate Costs

For informational purposes only, market indices show that fully qualified young drivers aged 17–20 face an average annual premium of £1,837, which scales downwards by roughly 42% upon accumulating your first year of clean No Claims History. To estimate your specific vehicle group brackets and source tailored market rates, utilize our interactive platform finder widget below:

vehicle Insurance Quote Engine

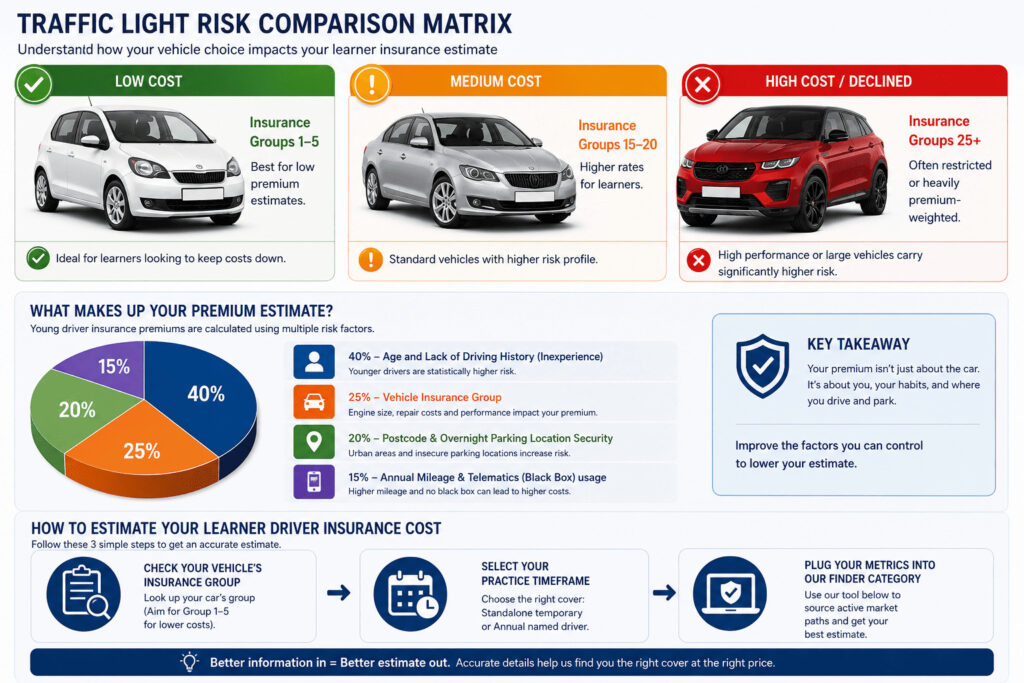

Choosing the Right Practice Vehicle: The Insurance Group System

If you are acquiring a personal vehicle to utilize during your learning lifecycle, or if your household contains multiple cars, selecting the correct vehicle asset is the single most critical decision you will make. The Association of British Insurers (ABI) allocates every passenger vehicle registered in the UK into an official Insurance Group numbered from 1 to 50. Group 1 comprises vehicles presenting the absolute lowest underwriting risk profile, while Group 50 holds ultra-high-performance supercars and luxury imports.

The Optimal Target: Groups 1 to 5

To secure the lowest possible rates for provisional insurance, focus your vehicle search entirely on entry-level models utilizing naturally aspirated, low-displacement engines (typically 1.0L to 1.2L). These vehicles feature low repair complexities and widespread parts availability. The leading low-risk models include:

- Hyundai i10 (SE or Advance Trim): Consistently holds Group 1 or 2 status, making it highly recommended for low premiums.

- Volkswagen Up! / Skoda Citigo / SEAT Mii: This trio of city cars features robust build quality, small engines, and low insurance group placements.

- Skoda Fabia (1.0L MPI variants): Offers excellent interior dimensions and practical utility while maintaining a Group 4 placement.

- Kia Picanto (Base Trim ‘2’): Backed by a strong warranty profile, this vehicle regularly delivers competitive provisional and young driver insurance quotes.

The High-Risk Zone: Avoid Groups 20 and Above

Do not attempt to secure learner coverage for premium saloons, executive estate cars, or mid-sized SUVs. Attempting to insure a provisional licence holder on a BMW 3-Series, an audi A4, a Land Rover Discovery, or any vehicle equipped with a turbocharger or performance modifications will trigger extremely high premium rates. In many cases, temporary underwriting software will reject the application entirely, citing strict internal risk caps.

Deconstructing Compulsory and Voluntary Excess Mechanics

During the configuration of any insurance policy, you will encounter the dual-layer system of insurance excess. The excess is the pre-agreed sum of money that you must personally pay toward vehicle repair costs before the insurance provider pays the remaining balance of the claim.

1. Compulsory Excess: This is a fixed, non-negotiable threshold determined solely by the insurer’s risk algorithm. Because provisional drivers lack real-world road experience, underwriters manage their exposure by applying a higher compulsory excess—frequently locked between £150 and £250—which cannot be lowered by the applicant.

2. Voluntary Excess: This is a flexible figure chosen by the applicant during the application phase. Opting for a higher voluntary excess (e.g., electing to shift it from £0 to £250) signals to the underwriter that you are willing to absorb more personal financial responsibility for minor cosmetic incidents. In response, the insurer’s pricing engine will lower your initial premium cost.

However, you must exercise caution. If you set your voluntary excess to £300 while your compulsory excess is fixed at £250, your total combined out-of-pocket obligation following a collision is £550. You must ensure this combined total is an amount you can genuinely afford to pay at short notice. For a comprehensive breakdown of how these components protect you following a serious road incident, refer to our detailed legal overview of what fully comprehensive car insurance covers in the UK.

The Legal Criteria for Supervising Drivers

Possessing a fully executed insurance policy document is only one component of remaining road-legal during private practice. Under UK statutory law, a provisional licence holder is forbidden from operating a vehicle on public roads unless they are actively accompanied by a qualified supervising driver who meets strict legal requirements.

If your accompanying supervisor fails to meet even one of the statutory criteria, your insurance policy is rendered void. This transforms your journey into an act of uninsured driving, exposing you to the full weight of roadside vehicle seizure and licence points.

The Statutory Minimum Milestones

According to current UK driving regulations, an individuals acting as a supervisor must adhere to the following rules:

- Age Thresholds: The absolute statutory minimum age is 21 years old. However, consumers must review their insurance policy small print carefully; many specialist short-term underwriting providers increase this internal risk requirement to 25 years of age.

- Licence Longevity: The supervisor must have held a full, valid driving licence from the UK, EU, or EEA for a minimum of 3 consecutive years. If their licence was suspended or revoked at any point during those three years, the continuous clock resets.

- Transmission Consistency: The supervisor must be legally qualified to drive the exact transmission variant being used for the practice session. If you are learning in a manual vehicle, your supervisor must hold a full manual licence. An individual who only holds an automatic licence cannot legally supervise a learner in a manual car.

Real-World Legal Obligations of the Supervisor

A supervising driver is not a passive passenger along for the ride. The law views the supervisor as the individual who maintains ultimate operational command of the motor vehicle. Consequently, they are bound by the same highway laws as if they were physically occupying the driver’s seat:

- Intoxication Status: The supervisor must remain strictly under the legal UK drink-drive limit. It is a serious criminal offence to accompany a learner driver while under the influence of alcohol or prescription drugs.

- Mobile Device Interaction: The supervisor is legally prohibited from using a handheld mobile phone, texting, or interacting with a tablet while the learner is driving. They must maintain constant visual focus on the road ahead to identify hazards and provide timely guidance.

- Visual Identification (L Plates): The supervisor must verify that official, regulation-sized red L plates (or D plates in Wales) are securely affixed to both the absolute front and rear exteriors of the vehicle. These plates must be clearly visible from a distance of 45 metres and must be physically removed or completely covered whenever the vehicle is being operated independently by a fully licensed driver.

Emergency Action Protocol: Incident Management During Practice

Even during highly structured, low-speed practice sessions with an attentive supervisor, collisions and minor motoring accidents can occur. Knowing how to manage an incident calmly ensures physical safety and protects your insurance position.

- Execute an Immediate Safe Stop: The instant a collision occurs, guide the vehicle to a safe position off the main driving lane if possible. Switch off the engine, activate your hazard warning lights, and apply the handbrake firmly. Under the Road Traffic Act, failing to stop at the scene of an accident is a criminal offence that carries severe penalties.

- Conduct an Immediate Injury Assessment: Check yourself, your supervising passenger, and occupants of any third-party vehicles for injuries. If anyone requires medical attention, or if the vehicles cannot be moved and create an active hazard to oncoming traffic, call 999 immediately.

- Do Not Admit Liability: When interacting with other motorists or witnesses at the scene, maintain a polite, neutral composure. Avoid apologizing, saying “I didn’t see you,” or making any statements that imply guilt. Admissions of fault made in the heat of the moment can legally compromise your insurer’s ability to defend your position during subsequent claims processing.

- Exchange Mandatory Information: You are legally required to exchange full names, telephone numbers, residential addresses, vehicle registration markings, and the names of your respective car insurance companies with all involved parties.

- Document the Physical Scene: Use your smartphone camera to capture high-resolution images of the vehicle damage, relative positioning, road signs, skid marks, and weather conditions. If independent bystanders witnessed the collision, request their contact information before leaving.

- File an Insurance Report: Notify your standalone learner insurance provider as soon as possible, ideally within a few hours of the incident. You must report the event to them even if the cosmetic damage is negligible and you choose not to proceed with a formal claim for repairs.

Four Strategic Methods to Cut Learner Premium Costs

While provisional motorists represent an elevated risk within underwriting databases, you can actively reduce your quotes by adopting specific, data-backed optimization tactics.

1. Harness the Power of Telematics App Technology

Telematics insurance, colloquially referred to as “black box” cover, replaces generic demographic risk assumptions with real-time driving data. By utilizing a small dashboard hardware device or a background smartphone application, the insurer monitors your speed adherence, braking smoothness, cornering g-forces, and seasonal driving times. Consistently practicing smooth, defensive driving styles demonstrates that you are a low-risk motorist, which can unlock lower renewal rates.

2. Optimize Job Description Vocabulary

When completing online insurance quotation engines, the precise terminology you select to describe your occupation can alter your risk score. Insurance software relies on historical claims data mapped to specific job titles. While you must always remain completely honest, explore variations that accurately describe your daily duties. Testing terms like “Clerical Assistant” versus “Office Administrator” can sometimes reveal a variation in pricing within underwriting software.

3. Choose Annual Upfront Payments for Personal Vehicles

If you have purchased a vehicle that you intend to use throughout your learning phase and keep after passing your test, buy an annual learner policy and pay the entire premium upfront. Opting for monthly installment payments is legally classified as entering into a consumer credit agreement with the insurer. This adds an interest markup that frequently carries an APR between 20% and 30%. Paying the lump sum upfront removes interest charges entirely.

4. Implement the Strategic Purchase Window Trick

Never purchase a temporary or annual insurance policy at the exact minute you intend to turn the ignition key. Underwriting analytics reveal that drivers who arrange their coverage 3 to 7 days in advance of their intended start date are statistically more organized and risk-averse than those who purchase instant cover at the roadside. Insurance pricing algorithms reward this organized behavior with lower premium quotes.

Additionally, remember that keeping your driving record pristine is essential for long-term affordability. Building a clean history during your provisional phase prevents future financial spikes; for example, avoiding early driving convictions ensures you won’t have to look up how much an SP30 speeding ticket increases car insurance later during your independent driving years.

Frequently Asked Questions (People Also Ask)

Can a provisional licence holder drive on a UK motorway?

Yes, but only under highly restricted statutory conditions. In England, Scotland, and Wales, learner drivers are legally permitted to drive on motorways only if they are accompanied by a fully qualified, Approved Driving Instructor (ADI) and are operating a vehicle equipped with dual controls that clearly displays official L plates. You are completely prohibited from entering a motorway during private practice with a parent or friend acting as your supervisor.

Does a temporary learner policy cover the actual driving test?

Yes. The vast majority of specialist standalone learner insurance providers include explicit comprehensive coverage for the duration of your official practical driving test. This allows you to complete the test within the familiar surroundings of your personal practice car rather than an instructor’s vehicle. During the practical test, the driving examiner is treated as your legal supervising driver under the terms of the policy.

Can I drive home from the test centre immediately after passing?

Absolutely not. This is a common legal trap that catches out hundreds of learners every year. The exact second the driving examiner hands you your passing certificate, your provisional driving licence status ends. Because your learner insurance policy is bound directly to your provisional status, the policy becomes completely void. You cannot legally drive home from the test centre using a learner policy. To drive home legally, you must contact an insurance provider via phone or app to upgrade your policy to a full young driver annual policy or buy a dedicated short-term qualified driver policy.

Can multiple learners share the same practice vehicle?

Yes, but they cannot share a single insurance policy document. If two siblings within the same household are practicing in a parent’s car, each individual driver must procure their own independent, standalone provisional insurance policy. The pricing, excess, and validation parameters will be calculated separately based on each individual’s specific age, medical disclosures, and background checks.

Are there night-time driving curfews on standalone learner policies?

While UK statutory law does not enforce a nighttime driving curfew on provisional licence holders, individual insurance underwriters frequently apply their own restrictions. Many short-term standalone policies contain an internal curfew clause that invalidates coverage between the hours of 10:00 PM and 6:00 AM to eliminate high-risk late-night driving environments. Always verify your policy wording before planning a late-night practice session.

The Road to Driving Success

Private driving practice is an invaluable tool for building your confidence, refining your hazard perception, and reducing the total number of professional lessons required to pass your test. By selecting a vehicle in a low insurance group, leveraging standalone short-term policies to protect your family’s No Claims Bonuses, and strictly following the rules of supervision, you can navigate your learning journey safely, legally, and within budget.

For official, up-to-date guidance on structural changes to licensing rules or testing standards, motorists can monitor updates on the GOV.UK Learning to Drive Portal.