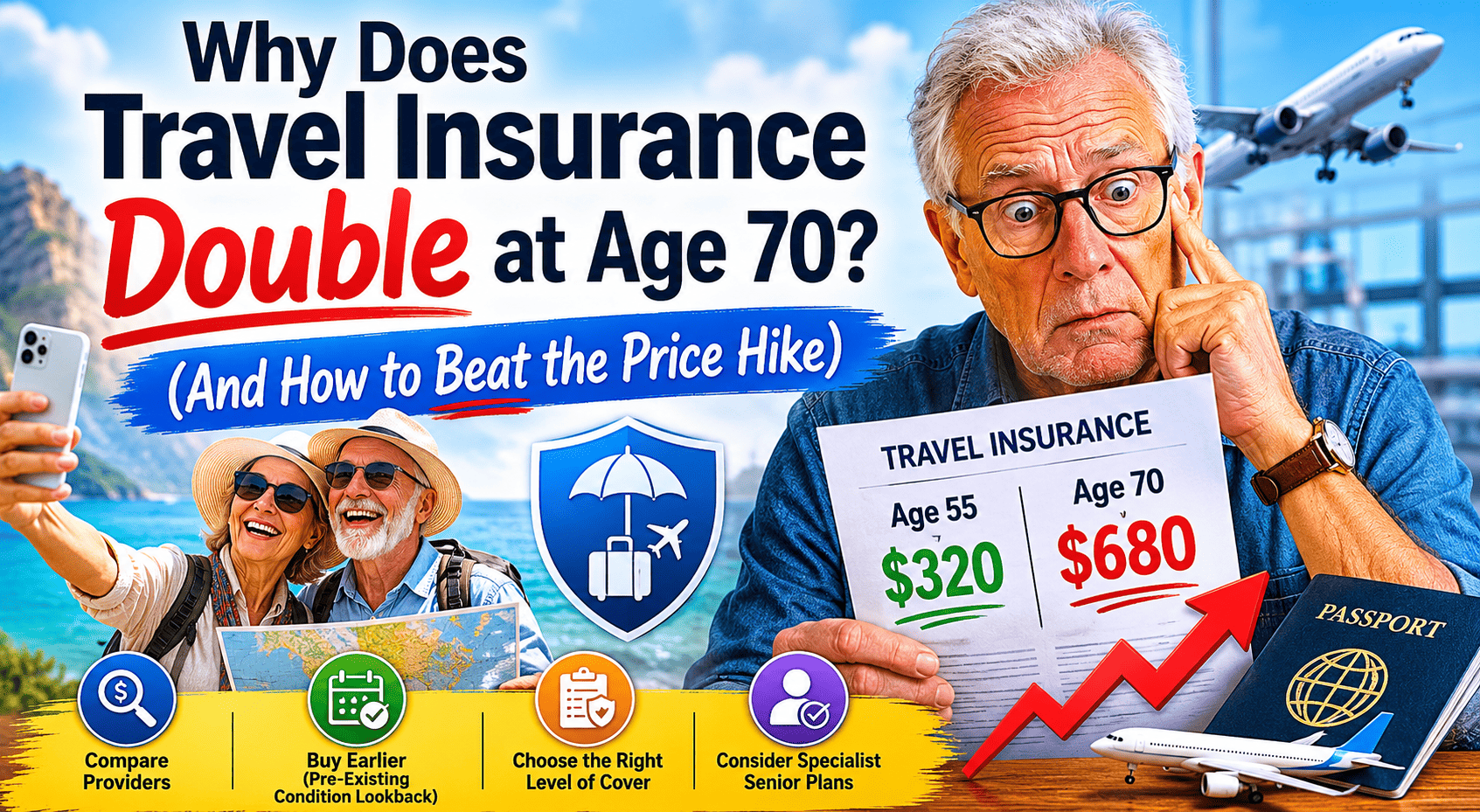

It is one of the most frustrating milestones in a British traveller’s life. You blow out the candles on your 70th birthday, you feel fantastic, you still walk the dog three miles a day, and you take no major medication. Yet, when the renewal notice for your holiday cover drops through the letterbox, the price has inexplicably surged.

You immediately jump online, trying to figure out the average over 70 travel insurance cost UK providers are currently charging, only to find that the automated comparison sites are treating you like a massive medical liability.

If you have just experienced a severe travel insurance price increase at 70, you are not alone, and you are not necessarily doing anything wrong. The UK insurance industry operates on a very rigid set of demographic algorithms. When you cross into a new decade, the computer stops looking at your personal fitness and starts looking at national statistics.

In this comprehensive 2026 guide, we are going to strip away the industry jargon. We will explain exactly why is travel insurance so expensive for over 70s, break down the actual market averages so you know if you are being overcharged, and give you six insider tactics to force the underwriters to lower your premium.

The Underwriter’s Secret: Why the Algorithm Punishes Your 70th Birthday

To understand how to beat the price hike, you first have to understand what the underwriter is actually afraid of. Insurance companies do not care if you run marathons or play golf every weekend. They only care about the financial risk of repatriation.

When you buy a policy, the cancellation cover (for lost flights and hotels) is just pocket change to the insurer. The real financial danger is the medical and repatriation section. If an under-65 breaks a leg in Spain, it costs the insurer a few thousand pounds. If an over-70 suffers a complex medical emergency abroad, the costs scale exponentially.

Here are the two primary reasons your age triggers a massive price hike:

1. The Cost of Medical Repatriation

If you require an air ambulance back to the UK from the Canary Islands with a full medical team onboard, the bill easily exceeds £15,000. If you require that same flight from Florida, the bill can breach £70,000. Statistically, the likelihood of requiring complex medical transport rises sharply after the age of 70. The insurer is simply front-loading that statistical risk onto your premium.

2. The “Undiagnosed” Risk Factor

You might declare a completely clean bill of health. But to a computer algorithm, a perfectly healthy 72-year-old represents an “undiagnosed risk.” Insurers worry intensely about sudden, unforeseeable age-related events—such as strokes or sudden cardiac events—that occur without any prior medical warning. Because they cannot price this risk based on your medical history, they price it based entirely on your date of birth.

The Hard Numbers: Average Over 70 Travel Insurance Cost UK

So, what should you actually be paying? If you are staring at a quote for £300 to go to France for a week, you need a realistic benchmark.

In the current 2026 UK market, pricing is heavily dictated by destination banding. Insurers divide the world into regions based entirely on how expensive their local hospitals are. Europe is relatively cheap. The USA, Canada, and the Caribbean are punishingly expensive.

| Trip Type & Destination | Average Cost (Age 70-74) | Average Cost (Age 75-79) |

|---|---|---|

| Single Trip: Europe (7 Days) | £35 – £60 | £55 – £85 |

| Single Trip: Worldwide (Excl. USA/Canada) | £70 – £120 | £110 – £170 |

| Single Trip: Worldwide (Incl. USA/Canada) | £150 – £250+ | £220 – £350+ |

Check Your Baseline: Over 70 Travel Insurance Calculator

Stop guessing and find out exactly what the market rate is for your specific trip. Use our independent over 70 travel insurance calculator below. Input your age bracket, your destination, and your trip length to instantly generate a realistic premium benchmark.

Over 70s Travel Insurance Estimator

Input your age bracket, your destination, and your trip length to instantly generate a realistic premium benchmark for an independent travel insurance policy.

*Disclaimer: All calculations provided by this tool are estimates for informational purposes only.

The Trap of Annual Multi-Trip Travel Insurance Over 70

For decades, the golden rule of holidaying was to buy a 12-month policy. It was the smart, economical choice. However, once you cross the 70-year threshold, buying annual multi-trip travel insurance over 70 often becomes a massive financial trap.

Here is how the pricing algorithm works for an annual policy: The computer must assume the worst-case scenario. It assumes you will travel to the most expensive destination within your chosen region, multiple times a year, for the maximum allowed duration.

If you buy a European annual policy, the insurer prices it as if you are spending 31 continuous days in a private Swiss clinic. In reality, you might just be taking a five-day city break to Rome and a week in the Algarve.

6 Insider Tactics to Slash Your Renewal Price

You cannot change your date of birth, but you can drastically change how the underwriter calculates your risk. If you are facing a massive premium hike, deploy these six strategies before you hand over your credit card.

1. Weaponise Your GHIC

If you are travelling within the EU, ensure you have a valid Global Health Insurance Card (GHIC) – the replacement for the old EHIC. This card grants you access to state-provided healthcare in EU countries at the same price a local resident would pay (often free). Many specialist insurers will waive the excess on medical claims, or offer a discounted premium upfront, if you agree to use public hospitals via your GHIC before turning to private facilities.

2. Carve Out the USA and Canada

North American healthcare operates on a privatised, profit-driven model. A single night in a US hospital bed can cost $5,000 before a doctor even looks at you. If you are buying a worldwide policy but you are only planning to visit Australia and Thailand, make absolutely certain you select “Worldwide Excluding USA, Canada, and the Caribbean.” Ticking the box that includes North America will instantly double or triple your premium.

3. Be Ruthless About Cruise Cover

Cruises are uniquely expensive to insure for the over 70s. If you suffer a heart attack on a ship in the middle of the Mediterranean, you cannot be put in an ambulance; you have to be airlifted off the deck by a helicopter. This is why “Cruise Extensions” add so much to a premium. If your holiday involves staying on dry land, explicitly ensure cruise cover is deselected on your quote.

4. Declare Everything (The Danger of Non-Disclosure)

Many older travellers try to keep costs down by “forgetting” to declare minor ailments like controlled high blood pressure or a routine statin prescription. This is a catastrophic error. If you fall ill abroad—even for something entirely unrelated, like a broken ankle—the claims handler will demand access to your UK medical records. If they discover an undeclared condition, they will void the policy entirely under the grounds of “non-disclosure,” leaving you personally liable for a £30,000 hospital bill.

5. Tweak Your Maximum Trip Duration

If you are forced to buy an annual multi-trip policy, look closely at the “maximum trip duration” limit. Most standard policies allow trips of up to 31 days. If you know you never go away for longer than a fortnight, use a provider that allows you to cap the maximum trip duration at 15 days or 21 days. Reducing this risk window can slice 10% to 15% off the final price.

6. Abandon the Mainstream Supermarkets

Firms like Tesco, Post Office, and Direct Line are excellent for 30-year-olds going to Ibiza. They are terrible for 75-year-olds going to Florida. Mainstream algorithms are highly restrictive. You need to pivot to specialist brokers who exist specifically to underwrite older travellers. Look for providers like Staysure, AllClear, Saga, or Avanti. They have their own medical screening algorithms that are far more forgiving of routine, age-related medications.

Frequently Asked Questions (FAQ)

Why do some insurers refuse to cover me at all after 75?

Many standard mainstream insurers have a strict upper age limit written into their underwriting rules, often capping out at 74 or 79. It is not a reflection of your personal health; it is simply because they do not have the specialist medical screening software or the reinsurance contracts to cover the statistical risks of older age groups. You must use a specialist senior broker.

If I am travelling with a younger partner, should we get a joint policy?

Rarely. If a 72-year-old and a 65-year-old buy a joint policy, many standard algorithms will price the entire policy based on the risk profile of the older, more expensive traveller. It is almost always cheaper for the 65-year-old to buy a standard mainstream policy, and the 72-year-old to buy a separate, specialist senior policy.

Does high blood pressure count as a pre-existing condition?

Yes. Even if your blood pressure is perfectly managed by a daily tablet and hasn’t caused you an issue in a decade, the fact that you require medication means it is a pre-existing medical condition. You must declare it. Fortunately, standard, well-managed hypertension rarely adds a significant amount to a specialist premium.