In the UK insurance ecosystem, an underwriting profile is calculated down to precise structural calculations. When you break ground on a modern single-story rear extension, alter a roofline, or introduce a flat roof structure, you are changing the underlying risk profile of your asset. If you fail to communicate these changes via an explicit disclosure notice, you risk finding out your entire multi-hundred-thousand-pound home policy has been quietly rendered void right when you need to make a claim.

This deep architectural and insurance breakdown explores exactly why structural alterations require formal notification, how underwriters view unique additions like modern flat roofs, and provides a secure, completely free tool to draft your insurance notification template automatically.

The Legal Realities: Why Prior Notification is Non-Negotiable

A standard residential home insurance policy is fundamentally a legally binding contract based on the principle of utmost good faith. Under the regulations set out in the UK’s Consumer Insurance (Disclosure and Representations) Act, homeowners hold an absolute duty to take reasonable care not to make a misrepresentation to their insurance providers. This legal framework means you are required to answer all questions accurately and promptly disclose any material changes to your property.

If you fail to notify your current insurer about structural building works or changes to your roof dimensions, you commit non-disclosure. If a major storm, accidental fire, or flash flood causes damage to your house—even on the completely opposite side of the building—the claims adjuster can cross-reference property records, spot the unnotified works, and deny the payout completely, leaving you personally liable for the repair costs.

Evaluating Risk Across the Two Phases of an Extension

Insurance companies do not simply assess your extension based on what it looks like when it is finished. Their underwriting teams split the timeline of your property renovation into two completely distinct risk profiles, layout details of which must be clearly defined in your written notice.

While contractors are active on your land, your house transitions from a standard family home into an active construction site. The baseline risks spike across several underwriting vectors:

- Structural Failure: Knocking through supporting bricks exposes foundations to shifting threats or localized collapses.

- Weather Exposure: Open structures leave home interiors vulnerable to water leaks from failed temporary tarping systems.

- Site Security: Scaffolding provides easy entry pathways to upper windows for opportunist burglars.

Once the contractors hand over the keys and the building control certificate is signed off, the long-term risk math changes entirely. The underwriter looks at permanent physical updates:

- Total Rebuild Value: Extensions add massive square footage, meaning original building sum insured amounts are no longer high enough to protect the asset.

- Structural Material Mix: Insurers track material parameters to establish baseline weathering indexes.

The Flat Roof Problem: UK Underwriting Realities

If your upcoming design includes a flat roof extension, you need to understand exactly how this shapes your underwriting file. Historically, flat roofs have been a source of major friction inside UK insurance firms. Decades ago, old felt-and-bitumen flat roof builds were notoriously prone to leaking, suffered accelerated wear due to UV degradation, and experienced severe structural stress from water pooling during typical British downpours.

Because of this, many standard home insurance providers still maintain strict limits in their policy wording. It is highly common to see a clause stating that if more than 20% or 30% of your home’s total roof area is flat, the property shifts into a “non-standard” underwriting category, which can trigger an automatic premium adjustment or an elevated policy excess for weather claims.

Modern flat roofing materials have evolved dramatically. If your extension utilizes high-performance systems, specify this clearly in your letter to maintain standard premium baselines:

- EPDM Synthetic Rubber: Incredible UV resistance and elasticity profile.

- GRP Seamless Fiberglass: Zero seams prevents structural water penetration vectors.

- Single-Ply Membranes: Industrial-grade lifespan exceeding 30 to 40 years.

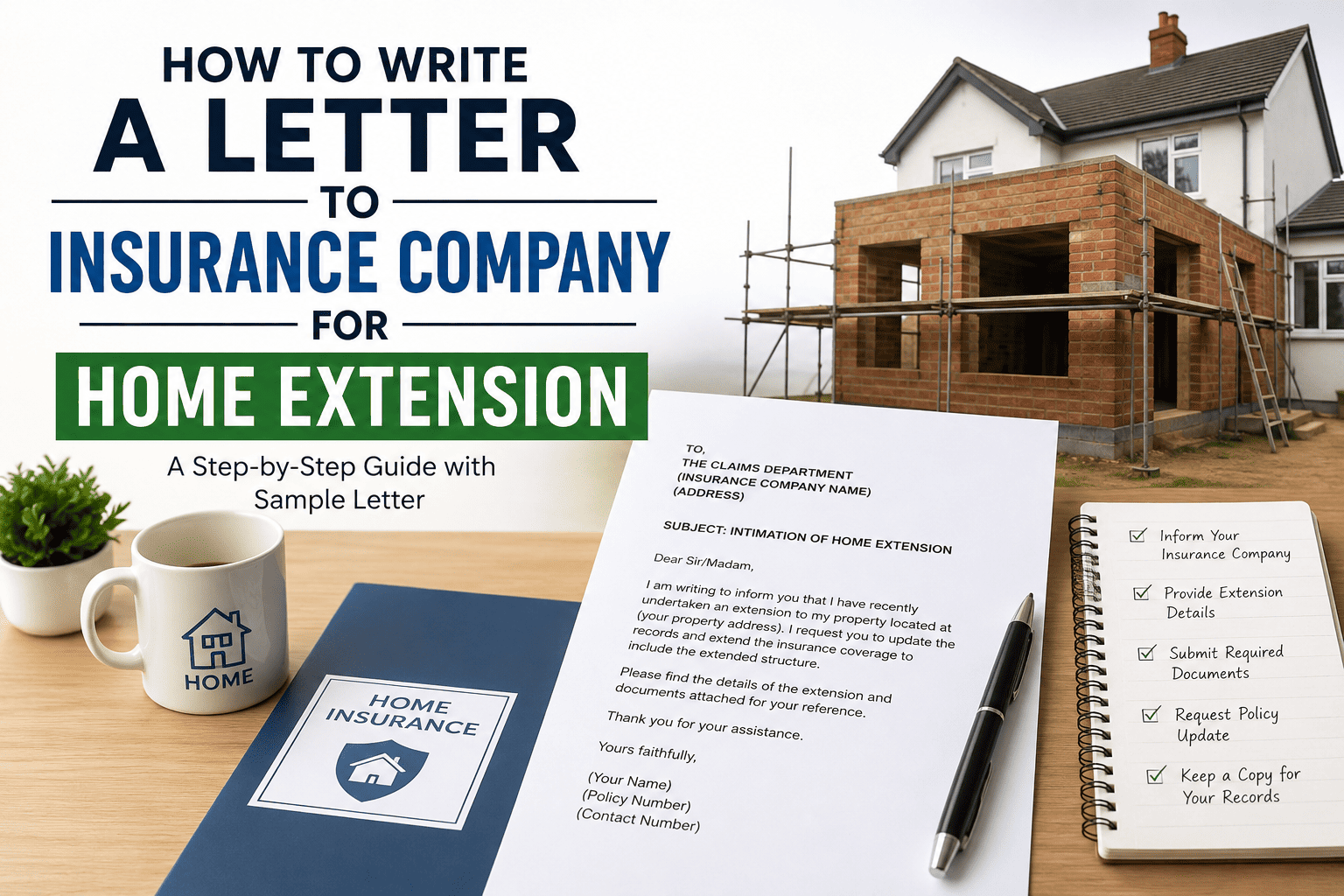

Your formal property alteration notification letter must cleanly explicitly specify the following contract items to prevent back-and-forth administration delays:

- Policy number and matching site address details.

- Exact contractor Public Liability values (Minimum £2m).

- Confirmed structural component materials.

- Property residency status during construction.

Secure Insurance Notification Letter Generator

Avoid formatting errors and confusing insurance jargon. Use our secure, localized generator tool to prepare a formal property alteration disclosure document for your insurer in seconds.

Insurance Letter Generator

*Disclaimer: All calculations provided by this tool are estimates for informational purposes only.

Understanding the Renovation Project Lifecycle

Managing your insurance through a structural alteration requires a step-by-step approach that coordinates with your build schedule. Below is the standard industry sequence for protecting your asset from pre-construction to final sign-off:

| Project Phase | Required Homeowner Action | Underwriting Purpose |

|---|---|---|

| 1. Pre-Groundbreak | Submit your formal declaration letter to your insurer at least 30 days before work begins on site. | Gives underwriters sufficient time to assess the structural risks and apply a formal “building works endorsement” to your file. |

| 2. Vetting | Obtain and review a valid copy of your contractor’s Public Liability Insurance certificate. | Ensures the builder’s policy assumes primary legal financial liability if their team accidentally compromises your home’s main foundations. |

| 3. Construction | Proactively notify your insurer if your timeline slips or if structural designs change mid-way through the build. | Maintains the validity of your temporary site endorsement and ensures coverage doesn’t expire mid-build. |

| 4. Practical Sign-Off | Provide your insurer with the final build dimensions, cost breakdown, and building control certificates. | Recalculates your permanent home rebuild valuation (sum insured) to ensure your expanded property is never underinsured. |

Advanced Insurance Concepts for Major Builds

For standard single-story rears or basic kitchen knock-throughs, your existing home insurer will usually be happy to extend your coverage by applying a temporary premium modification or an endorsement to your active policy. However, if your extension project scales up in complexity, you may encounter advanced insurance requirements:

JCT Contracts & Party Wall Agreements

If you are signing a standard Joint Contracts Tribunal (JCT) agreement with your builder, or if your extension sits on a boundary line requiring a Party Wall Act agreement, your insurer must know. Certain JCT clauses require you to insure the existing structure and the new works jointly in both your name and the contractor’s name, which requires a specialist policy adjustment.

Non-Standard Renovation Insurance

If your project involves a deep basement excavation, a massive multi-story addition costing over £100,000, or if the structural modifications are so severe that you must move out of the house for months, your standard provider may choose to suspend your coverage temporarily. In this scenario, you will need to put a specialist Renovation Insurance policy in place.

Frequently Asked Questions

Will my home insurance premium automatically go up when I build an extension?

During the actual construction phase, your premium may not rise significantly, although most UK insurers will charge a small, fixed administrative processing fee to log the building endorsement. Once the extension is fully complete, however, your premium will generally adjust upward to reflect the fact that your home now has a larger footprint, more liveable rooms, high-value fixtures, and a higher overall structural rebuild value.

What is the difference between non-disclosure and misrepresentation?

Non-disclosure happens when you completely omit or forget to mention a major structural change, like building an extension without alerting your provider. Misrepresentation occurs when you actively supply incorrect details—such as telling your underwriter your new extension has a pitched slate roof when it actually features a flat timber-and-felt configuration. Both give your insurer a legal path to instantly cancel your policy and deny claims.

Do I need to inform my contents insurance provider as well as my buildings insurer?

Yes. A home extension frequently means adding a new kitchen, high-end electronics, or new furniture sets, which substantially increases the total replacement value of your personal possessions. Furthermore, during construction, your items are exposed to higher risks of dust, accidental damage, or theft due to the contractors on site. Both elements of your policy must be reviewed together.