For a UK property investor, an empty building is traditionally viewed through a purely financial lens: it represents lost yield, ongoing council tax liabilities, and marketing expenses. However, within the specialist insurance markets of the City of London, a vacant terrace house, suburban semi, or city-centre flat undergoes a dramatic risk reclassification the moment it becomes devoid of human habitation.

The underlying mechanics of residential property protection rely on regular occupancy to mitigate risk. When a tenant moves out, a property’s vulnerability profile shifts entirely. According to 2026 data from property management specialist Rushbrook & Rathbone, the average void period in England stands at 24 days, costing property owners an average of £1,135 in lost rent per vacancy. In higher-rent areas like London, that cost scales to £1,252 per void. When these natural transitions or unexpected life events push past the one-month mark, standard coverage fails. Understanding how underwriters view this shift—and knowing how to correctly leverage landlord insurance for unoccupied property uk—is what separates protected portfolios from catastrophic, uninsured financial losses.

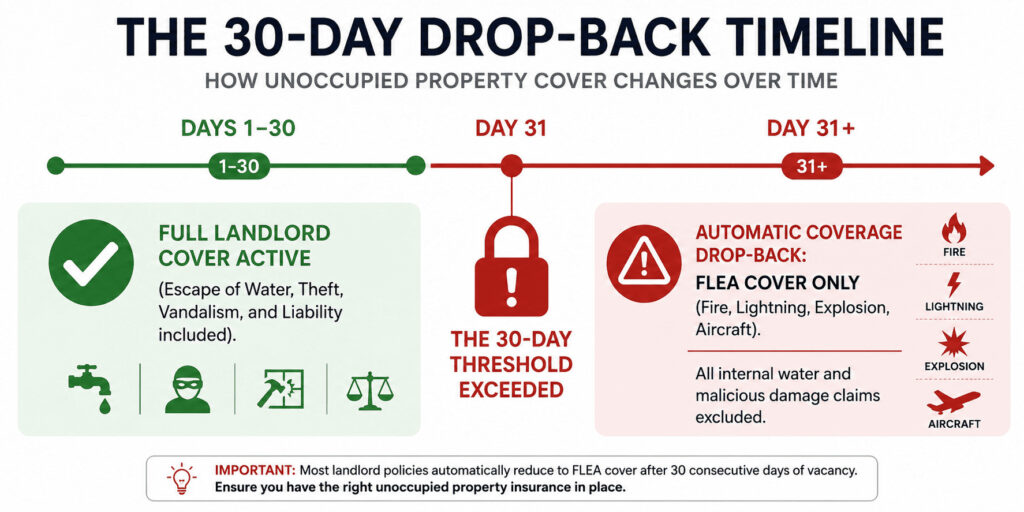

The Anatomy of an Insurance Crux: Why Standard Policies “Drop Back”

The central misunderstanding among many property owners is the belief that a premium paid guarantees absolute protection under all circumstances. Standard residential landlord policies operate under explicit assumptions. When those assumptions change, the contractual terms automatically adjust through standard policy endorsements.

The Consequence of the 30-Day Threshold

The vast majority of standard UK letting policies contain an unoccupancy limitation clause, typically benchmarked at 30 consecutive days (though select non-standard contracts may extend this to 45 or 60 days). Once the final tenant leaves and this clock expires, the insurer’s liability parameters contract sharply.

This process is known in the industry as a coverage drop-back. The comprehensive protection you rely on dissolves, leaving behind a bare-bones framework known colloquially as FLEA cover:

- [F] ire

- [L] ightning

- [E] xplosion

- [A] ircraft Impact

If an empty property suffers an arson attack, your FLEA policy will generally respond. However, if an intruder smashes a side window, enters the property, and turns on the taps to deliberately flood the floorboards, this is classified as Malicious Damage or Escape of Water. Under a dropped-back policy, the claim will be summarily denied. Dedicated unoccupied property insurance exists specifically to bridge this severe liability gap.

Deconstructing the Tiers of Unoccupied Coverage

When arranging specialized cover for an empty building, a broker will not simply offer a one-size-fits-all policy. Instead, they evaluate the asset against distinct operational tiers. Selecting the appropriate tier requires balancing your risk tolerance against your renovation budget or transition timeline.

Tier 1: Perils Ex-Water, Theft, and Malice (PETM)

This mid-tier option covers major atmospheric events—such as localized flooding, severe storms, or subsidence—while intentionally omitting the three most common human-centric risks associated with empty properties: theft, vandalism, and internal pipe failures. It is typically utilized for properties that are entirely stripped of fixtures and awaiting structural demolition or total rebuilds.

Tier 2: Comprehensive Unoccupied Perils

The gold standard for asset protection, this tier reinstates full protection for Escape of Water (EoW), malicious mischief, and theft. However, because these risks are exceptionally high in empty structures, securing this level of coverage requires absolute compliance with specific, non-negotiable operational conditions set by the underwriter. Recent 2026 insurance market indexes show that the median annual cost of landlord insurance sits around £285 for standard operational properties, but shifting an asset into a comprehensive unoccupied tier typically increases the risk premium by 30% to 50% due to the statistical likelihood of severe hidden claims.

Underwriting Compliance: The Hidden War Rules of Vacant Property Management

Specialist unoccupied policies are highly conditional contracts. The underwriter accepts an elevated risk profile on the condition that the landlord acts as a proactive risk manager. Failure to strictly execute these mandated operational duties can invalidate the entire policy, rendering coverage void at the exact moment a claim is filed.

1. The Auditable Inspection Regime

Insurers will not protect a property that is abandoned to the elements. Most policies feature a strict endorsement requiring a physical internal and external walkthrough every 7 to 14 days.

Crucially, this cannot be a casual glance from a car window. You, your letting agent, or a designated property manager must physically enter the premises and log the visit. In the event of a significant loss, a loss adjuster will demand an inspection log. To ensure validity, maintain a digital diary containing:

- The exact timestamp of entry and exit.

- A signed declaration confirming the integrity of the roof, windows, and boundaries.

- Photographic proof of key areas (such as the loft hatch and stopcock area) to establish a clear timeline of maintenance.

2. The Winter Utility Mandate (October to April)

The UK winter brings a severe threat of freezing pipes, which can cause devastating structural damage if water flows unchecked for days. Unoccupied property underwriters combat this with binary utility clauses during the colder months:

Option A: Total System Drain-Down Shut off the mains water stopcock and have a professional plumber fully drain all heating lines, hot water cylinders, and tanks so no water remains to freeze.

Option B: The Constant Climate Rule Keep the gas and electricity utilities active, maintaining the central heating thermostat at a continuous temperature (usually between 12°C and 15°C) 24 hours a day to prevent freezing.

Failing to strictly execute one of these two methods means that any winter claim involving an escape of water will almost certainly be rejected for non-compliance with policy warranties.

3. Physical Security and Perimeter Enforcement

Insurers expect a higher standard of physical security than a simple night-latch. Standard requirements include installing 5-lever mortice deadlocks conforming to British Standard 3621 on all external wooden doors, or multi-point locking systems on uPVC doors. Windows on the ground floor or those accessible via flat roofs must be fitted with key-operated locks, and all keys must be removed from the property during the void period.

Scenarios That Demand Specialized Cover

Void periods are rarely identical. Identifying the specific catalyst behind your property’s vacancy allows you to source flexible short-term policies (typically available in 3, 6, or 12-month increments) rather than overpaying for a rigid, standard annual commitment.

The Capital Appreciation Project (Renovations and Building Works)

When modernizing an older UK property to increase its rental yield, standard landlord insurance falls short. If walls are being moved, plaster is drying, or rewiring is underway, you need an unoccupied policy that explicitly permits minor or major works.

It is critical to remember that any physical alterations to the building’s footprint or layout will permanently alter its underlying underwriting profile. If you are adding space during this void period, review our guide on how an extension affects home insurance in the UK to avoid unintentionally voiding your long-term cover. Furthermore, if your design plans include contemporary building materials, specialized structural layouts like a flat roof require careful underwriting attention. Be sure to evaluate how a flat roof extension impacts home insurance rules before contractors sign off on the design.

Important Portfolio Strategy: Ensure your main building contractor carries substantial Public Liability Insurance (minimum £5 million). If a contractor accidentally cuts through a gas line or causes a structural collapse, your unoccupied property policy will look to subrogate the claim directly to the contractor’s commercial insurer.

The Probate Transition

When a property owner passes away, assets often sit empty for months while executors navigate the UK courts to secure a Grant of Probate. Executors hold a strict fiduciary duty to safeguard the estate’s physical assets. For detailed guidance on your legal responsibilities during this transition, you can consult the official GOV.UK Probate Application Portal. Arranging specialized unoccupied cover under the name of “The Executors of [Deceased’s Name]” prevents personal financial exposure and keeps the property secure until it can be liquidated or transferred to beneficiaries.

The Structural Defect Void (Subsidence or Treatment)

Occasionally, a property becomes unachievable to let due to structural issues, such as historical subsidence requiring underpinning, or severe dry rot treatment. During these lengthy remediation phases, standard insurers will rapidly exit the risk. If an insurer cancels or alters your coverage unfairly during this process, landlords have the right to escalate the dispute to the Financial Ombudsman Service for an independent assessment. However, your immediate step should always be securing a specialist non-standard underwriter who understands how to price a policy for a building actively undergoing structural stabilization.

Macro Trends: The Shifting 2026 Regulatory Landscape for UK Landlords

The operational environment for UK property investors is undergoing its most significant shift in a generation. The implementation of housing reforms, alongside evolving economic pressures, has directly impacted the frequency and duration of property void periods—making specialized insurance coverage more critical than ever.

The Abolition of Section 21 and the Rise of Periodic Tenancies

Following historical legislative updates, the private rented sector has transitioned entirely away from fixed-term tenancies to rolling periodic structures. For property owners, this means predictability is down. Tenants now hold the right to give a standardized two months’ notice at any stage of their tenancy. While this gives renters flexibility, landlords face less control over the timing of transitions. A tenant exit can easily occur during low-demand winter months, significantly increasing the likelihood that a property hits the 30-day unoccupancy mark before a suitable replacement is referenced and moved in.

Longer Void Horizons Due to Compliance Red Tapes

Because the modern regulatory framework demands flawless local council licensing, structural efficiency benchmarks, and rigorous safety certifications before a new tenancy agreement can legally execute, turnover works are taking longer. Remedial works to address damp, upgrade insulation, or replace consumer units can easily keep a property offline for 6 to 8 weeks. Attempting to hide this vacancy timeline from your standard insurer is a profound breach of contract; you must transition to an unoccupied asset framework to keep your underlying equity insulated from unexpected claims.

Financial Analytics: Evaluating the Hidden Cost of a Property Void

Many landlords undercalculate the actual economic drain of a property remaining dark. They focus entirely on the headline figure of lost rent, failing to account for the secondary, compounding maintenance and compliance cash outflows that occur behind the scenes.

| Expense Class | Operational Status Cost (Per Month) | Unoccupied Status Cost (Per Month) | Primary Driver of Expense Change |

|---|---|---|---|

| Building Insurance | £24.00 | £36.00 to £50.00 | Risk scaling due to lack of manual site management. |

| Council Tax Liability | Covered by Tenant | £120.00 to £250.00 | Removal of empty property discounts by most local authorities. |

| Utilities Standing Charges | Covered by Tenant | £45.00 to £110.00 | Mandated minimum winter climate settings or basic draw. |

| Site Safety Auditing | £0.00 (Self-monitored) | £30.00 to £80.00 | Independent professional check fees or travel logging costs. |

When these data points are combined with continuous mortgage interest charges, a three-month void on an average UK terraced home can easily cause a net cash drain exceeding £3,500. Attempting to preserve margins by choosing cheap, basic FLEA coverage or failing to notify your underwriter leaves you exposed to a total loss scenario if a major structural incident strikes your asset.

Calculate Your Landlord Insurance Estimate Quote

Avoid the 30-day unoccupancy trap. Use our calculator to run an estimate quote. We do not sell insurance or show live provider quotes—our tool gives you a simple estimate of how much landlord insurance will cost for your property.

property Insurance Quote Engine

Actionable Risk Mitigation for Savvy Portfolio Managers

Securing competitive premiums for landlord insurance for unoccupied property uk requires demonstrating to the broker that you are an organized, low-risk client. For a comprehensive overview of how insurance firms handle risks, check the guidelines set by the Financial Conduct Authority (FCA), which regulates UK financial markets to ensure fair terms for consumers.

Implement this operational checklist during any property void to naturally deter criminals, minimize physical risks, and position your portfolio favorably during underwriting assessments:

- Implement Digital Interventions: Use smart, Wi-Fi-enabled timers on internal lamps to mimic irregular evening occupancy patterns rather than predictable mechanical timers.

- Enforce Mail Redirection: An overflowing letterbox is the primary indicator used by squatters and burglars to identify a vacant home. Install an internal post-catcher or clear the mail regularly.

- Maintain Exterior Curb Appeal: Keep front gardens trimmed and external paths clear. A property that looks actively managed is significantly less likely to attract fly-tipping or opportunistic vandalism.

- Secure Peripheral Boundaries: Padlock side gates and repair broken fence panels immediately to restrict back-access to the structure.

- Install Smart Multi-Sensor Alarms: Modern cellular-backed smart alarms can detect sudden temperature drops or humidity spikes, warning you of an imminent frozen line or roof leak before it escalates into a catastrophic structural claim.

Final Perspective

In the modern UK property market, a void period is an unavoidable operational reality. However, allowing a property to cross the critical 30-day threshold without transitioning to a dedicated unoccupied policy is a high-stakes gamble with your equity. By understanding underwriting expectations, maintaining strict inspection routines, and selecting the appropriate level of peril coverage, you can easily protect your investment through any transition.