It really starts with quite a normal trip to the vet. Your dog starts to limp after a walk or your cat stops eating and needs blood tests. Then the estimate arrives, and a typical everyday concern suddenly becomes a very difficult financial choice.

That’s the issue that pet insurance UK policies aim to solve. You pay a monthly or yearly premium, and the insurer will help with eligible veterinary expenses when your dog or cat has a covered accident or illness. The key word here is ‘eligible’. Pet insurance isn’t some sort of limitless cheque – and even the most affordable policy could turn out to be rather pricey if its limitations, excesses or exclusions don’t quite fit your pet’s requirements.

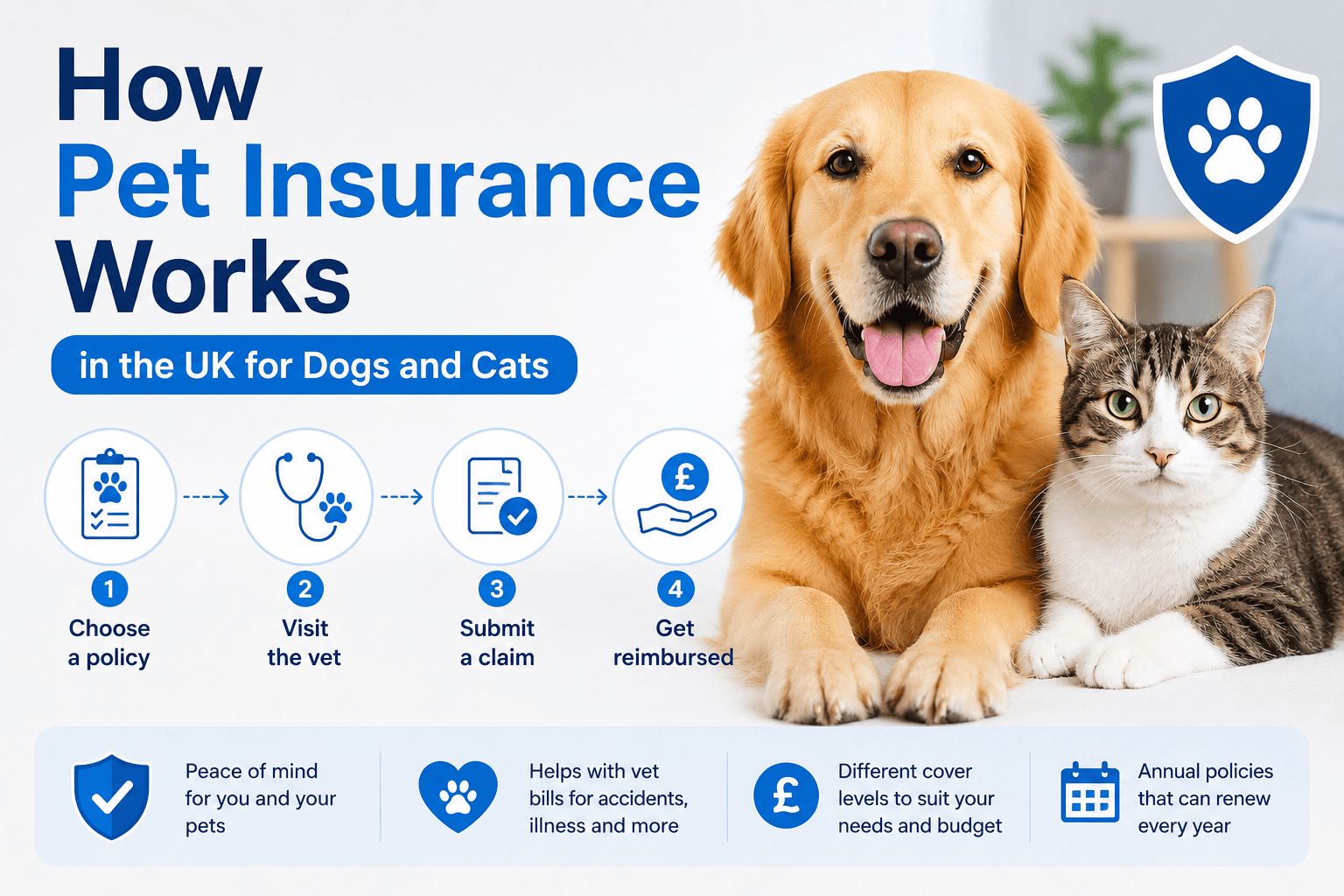

How does pet insurance work in the UK?

You choose a policy, veterinary fee limit and excess. The insurer prices it using factors such as your pet’s species, breed, age, postcode and medical history. Dogs often cost more to insure than cats, while some pedigree and flat-faced breeds attract higher premiums because certain health problems are more common.

Once cover begins, there may be an initial waiting period. If an illness or symptom appears during that period, the insurer may treat it as pre-existing and decline related claims. Buying cover while a pet is young and healthy can therefore be valuable.

When treatment is needed, the process usually works like this:

- You contact a vet and approve the treatment.

- You check whether the condition and treatment are covered.

- You or the vet submits a claim with invoices and clinical notes.

- The insurer assesses it against the policy wording.

- You pay the excess, any percentage contribution and anything above the limit.

- The insurer reimburses you or, where agreed, pays the vet directly.

Direct claims are not guaranteed. You may need enough cash or credit to pay the vet first.

The four main types of pet insurance

The policy type determines how long a condition remains covered and when the limit runs out. This matters far more than the headline premium.

| Policy type | How the cover works | Good for | Main trap |

|---|---|---|---|

| Lifetime | annual vet fee limit can refresh at renewal if cover stays continuous. | chronic or recurring conditions | Premiums can rise and all renewal terms still apply. |

| Maximum benefit | fixed total sum is available for each condition. | mid-level protection | Cover ends for that condition when its pot is used. |

| Time-limited | each condition has a time limit and usually a money limit. | lower-cost short-term cover | Treatment stops when the first limit is reached. |

| Accident-only | covers eligible accidental injuries, not illnesses. | basic emergency protection | Disease & chronic illness are excluded. |

Lifetime cover offers many owners the best protection from long-term conditions – diabetes, arthritis or chronic skin problems. The veterinary fee limit usually gets refreshed with each renewal, assuming that you do this without taking a gap and continue doing what’s required.

Maximum benefit and time-limited policies create a stopping point. Once the money or time allowance for a condition is exhausted, future treatment becomes your responsibility. Accident-only cover can protect against sudden injuries, but it will not usually help with illness.

What does pet insurance normally cover?

The core of most pet insurance UK policies centres on veterinary fees for accidents and illnesses. Depending on the product, coverage might include tests, surgery, hospital care, prescribed medication, physiotherapy – and dental treatment required because of an accident or illness.

More all-encompassing policies could add third-party liability for dogs, advertising and reward costs when a pet goes missing, boarding fees if the owner is hospitalized, emergency care abroad, behavioural treatment and end-of-life benefits. Third-party liability is far from a normal part of cat insurance plans.

What is usually excluded?

Most pet insurance UK policies exclude routine and predictable costs. Vaccinations, flea and worm treatment, grooming, routine check-ups, neutering and elective procedures are commonly paid by the owner. A veterinary health plan can spread some routine costs, but it is not insurance.

The biggest exclusion is pre-existing conditions. This could be a diagnosed illness, old injury, recurring symptom or clinical sign documented before cover started. Even a note in the veterinary history will affect a later claim if the insurer thinks it relates to the same underlying problem.

Other very common restrictions are dental claims where recommended care was missed, pregnancy and breeding costs, preventable illness where vaccinations weren’t always up to date, food and supplements, and behavioral or alternative treatments without a referral from a veterinarian.

Read the policy wording, not just the comparison page. The Financial Ombudsman Service sees disputes involving pre-existing conditions, dental exclusions, time limits, co-payments and changes to lifetime policies.

How excesses and co-payments change the claim

The excess is the amount you contribute towards an accepted claim. It may apply once per condition, once per policy year or each time you claim.

Imagine a fairly common £2,000 claim with a £100 excess and a 20% co-payment. It all depends on the policy wording – you might have to pay the £100 plus 20% of the remaining £1,900, resulting in your total outlay being £480.

Pets getting older are significantly more likely to incur percentage contributions. A lower premium may seem very appealing – right up until there’s a massive claim involved; so compare your potential overall outlay, not just the monthly price itself.

Dogs and cats are priced differently

A cat kept mainly indoors presents a different risk from an active dog that meets traffic, people and other animals. Dogs can also create third-party liability claims.

Breed matters. Certain dogs are quite susceptible to joint, spinal, respiratory or skin conditions. Some pedigree cats may have inherited heart, kidney, or respiratory problems. If you’re an owner of a flat-faced dog then you should very closely read about hereditary and congenital health issues.

Our guide to French Bulldog insurance costs explains why breed risk can transform both the premium and the cover needed.

Age is equally important. Premiums usually rise as pets get older, and insurers may add a co-payment or restrict new applications. Switching later can be difficult because recorded conditions may be excluded by the new insurer.

What Reddit owners repeatedly warn about

UK pet owners discussing insurance on Reddit return to three practical problems. Premiums can rise sharply as a pet ages, switching after a diagnosis may remove cover for that condition, and small claims can be poor value once the excess is deducted.

These are anecdotes, not a substitute for policy wording, but the pattern is useful. Insurance works best as protection against bills that would seriously damage your finances, not as a way to recover every routine expense.

Some owners self-insure through a dedicated savings fund. This can work when substantial money is available immediately. It is riskier when the fund is small because an accident or diagnosis can happen before enough has accumulated. The key question is whether you could fund urgent treatment tomorrow without unaffordable debt.

Get Your Pet Insurance Quote

Ready to protect your cat or dog? Use our quick comparison tool below to get a tailored policy estimate for your pet:

pet Insurance Quote Engine

How to choose a pet insurance policy

Start with the veterinary fee limit and policy type, then work backwards to the premium. Check whether the limit is annual, per condition or total. Confirm how chronic and hereditary conditions are treated and how the excess changes with age.

Check the claims process too. Find out whether your vet can claim directly, what evidence is needed and how quickly paperwork must be submitted. Compare several routes because no single comparison site covers every insurer.

A pet insurance estimate can provide a useful benchmark, but choose on cover rather than price alone.

Finally, disclose the medical history accurately. If a question is unclear, ask the insurer and keep the answer in writing.

Frequently Asked Questions

Is pet insurance compulsory in the UK?

No. Pet insurance is really optional. Owners of dogs can still be held accountable by law if their animal hurts someone – or destroys some property – so third-party liability cover might be a very good idea indeed.

Does pet insurance cover vaccinations and neutering?

Usually not. These are just routine or preventative expenses. Veterinary health plans will often help you pay them out over time – but they’re quite different from standard coverage for accidents and illnesses.

Can I change pet insurer every year?

Yes, but switching can create new exclusions. Conditions, symptoms or injuries recorded under the old policy may be treated as pre-existing by the new insurer.

Will a lifetime policy cover a condition forever?

It will continue covering an eligible condition whilst the policy is renewed uninterruptedly – and its limits, premiums, and terms are all met. It doesn’t usually cover conditions existing prior to the policy’s commencement.

Is pet insurance worthwhile for an older dog or cat?

It very much depends on the renewal cost, excess, co-payment, present cover and your power to self-fund any treatment yourself. Before dropping coverage, check which ongoing conditions will be left permanently uninsurable.

The bottom line

Lifetime, maximum benefit, time-limited and accident-only policies really differ quite a bit when your dog or cat develops a serious or recurring condition.

The best policy isn’t always the one with the biggest headline limit or lowest monthly premium. It’s the one that makes sense – both its limits, exclusions, and excesses – once a real vet’s bill actually shows up.