It is the moment every family simultaneously anticipates and dreads. The driving test has been passed, the L-plates have been ripped up, and the open road awaits. But the celebration often comes to a grinding, stressful halt the exact second you run a quote for first-time car insurance.

If you are staring at a screen displaying a premium that costs more than the vehicle itself, take a deep breath. You are not alone, and the system is not broken—it is just entirely driven by risk statistics.

Whether you are an 18-year-old trying to fund your own independence, or a parent trying to get your child on the road without taking out a second mortgage, navigating the UK motor insurance market requires strategy. In this comprehensive guide, we will break down exactly what the average car insurance cost for a young driver in the UK actually is, explain why underwriters charge so much, and give you seven legal, proven methods to drastically reduce your premium.

What is the Average Car Insurance Cost for a Young Driver in the UK?

In the UK insurance market, “young” typically refers to anyone under the age of 25, but the absolute peak of premium pricing hits drivers between the ages of 17 and 19. Recent industry data highlights a stark reality for new drivers entering the market. While prices fluctuate based on the quarter and inflation, here is what you can expect the average fully comprehensive annual premiums to look like:

| Age Bracket | Average Annual Premium (Fully Comprehensive) |

|---|---|

| 17 – 19 years old | £1,400 – £1,950 |

| 20 – 24 years old | £950 – £1,150 |

| 25 – 29 years old | £700 – £850 |

| UK National Average (All Ages) | £500 – £560 |

Note: These are medians. A 17-year-old living in a high-crime city center trying to insure a modified hatchback could easily see quotes exceeding £3,000, while a 19-year-old in a quiet rural village with a 1.0L engine might secure a policy for closer to £1,200.

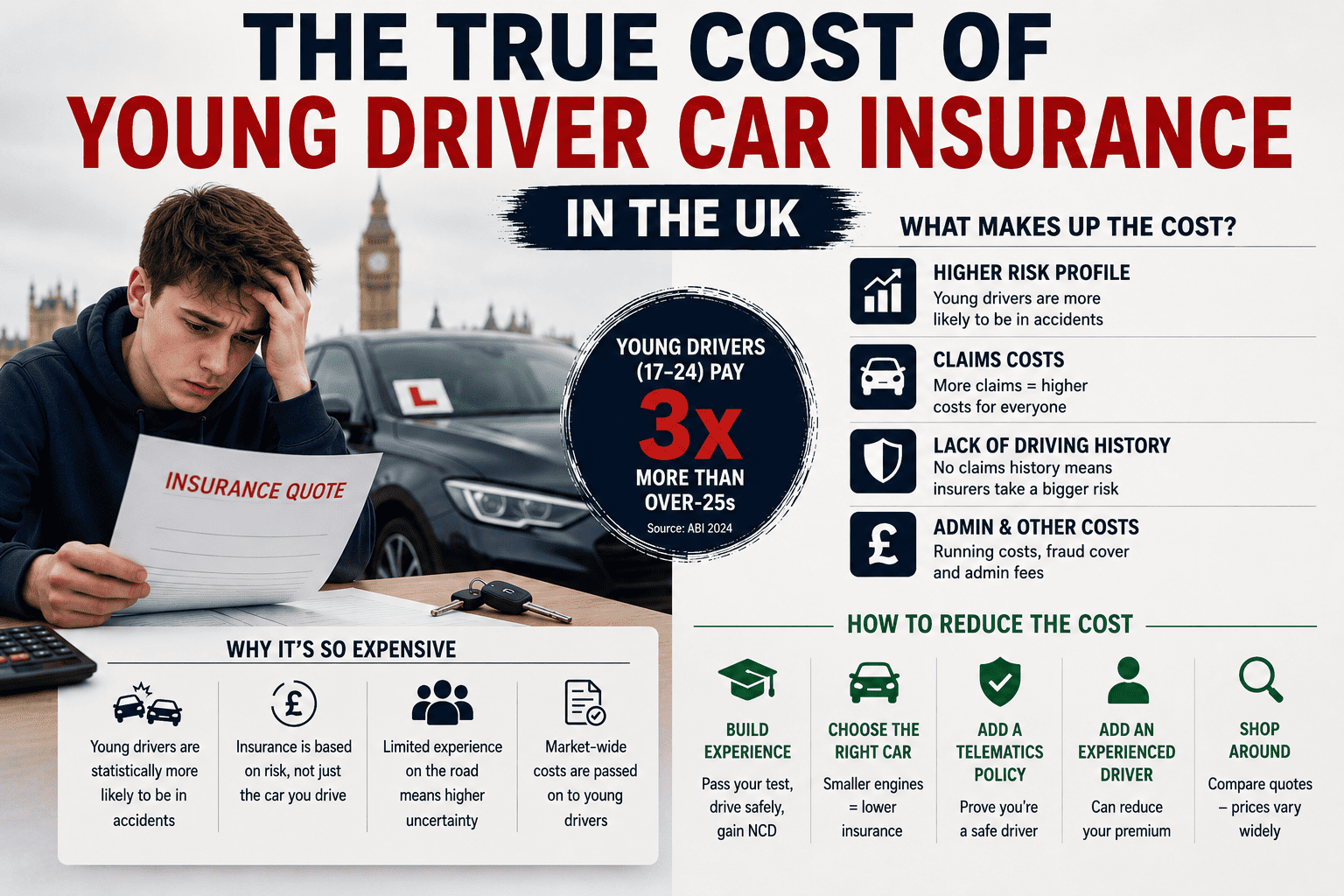

Why is First-Time Driver Insurance So Expensive?

It is easy to feel like insurers are actively trying to punish young people, but the pricing model is entirely mathematical. Insurers look at historical claims data, which paints a very specific picture:

- The Risk of Severe Accidents: Drivers aged 17 to 24 make up a relatively small percentage of total license holders but are involved in a disproportionately high number of serious crashes.

- Lack of Driving History: With zero years of driving experience and zero years of No Claims Bonus (NCB), the insurer has no track record to judge your personal safety.

- The Cost of Repairs: Modern cars are essentially rolling computers. A simple bumper scrape that used to cost £150 to fix now involves replacing parking sensors and recalibrating cameras.

Get Your Personalised Estimate

Before we dive into how to lower your costs, find out exactly what your baseline is. Use our intelligent estimator tool below. By inputting just a few basic details, our calculator uses current UK market logic to give you a realistic premium range.

vehicle Insurance Quote Engine

7 Proven Ways to Lower Young Driver Car Insurance Costs

You cannot change your age, and you likely cannot change your postcode. However, you have total control over several other massive rating factors. Here is how you beat the algorithm.

1. Embrace the Black Box (Telematics)

If you are under 20, a telematics policy is almost mandatory if you want a reasonable price. A “black box” is either a small device fitted behind your dashboard or an app on your phone that monitors your speed, braking harshness, cornering, and the times of day you drive. By proving to the insurer that you drive safely, you can instantly shave between 10% and 25% off your initial premium.

2. Be Strategic About the Vehicle (The Hand-Me-Down Trap)

Passing down a heavier, more powerful family vehicle—like an older SUV or estate car—can backfire spectacularly. They sit in much higher insurance groups. If you want cheap insurance, you must look at cars in Insurance Groups 1 to 5. Examples include the Volkswagen Up!, Hyundai i10, Toyota Aygo, or a 1.0L Ford Fiesta.

3. Add an Experienced Named Driver

Adding a parent or an older sibling with a clean driving license to the policy as a “named driver” can significantly reduce the premium, as the insurer assumes the risky driver is behind the wheel less often.

4. Tweak Your Job Title

Did you know that a “Chef” generally pays more for car insurance than a “Cook”? Or that a “Retail Worker” might pay a different rate than a “Shop Assistant”? Use a legitimate, accurate synonym for your role to see if it reduces the premium. Never lie about your occupation, but do explore all valid descriptions.

5. Location and Parking Security

If you have a driveway or a cleared-out garage, use it. Make sure you select “Kept on a Driveway” on the quotation form, as it lowers the risk of opportunistic theft and side-swipe vandalism compared to parking on a public road.

6. Do Not Wait Until the Last Minute

The “sweet spot” for buying car insurance is between 20 and 26 days before you want the policy to begin. Buying your policy on the exact day you want it to start suggests to the algorithm that you are disorganized and statistically more likely to have an accident.

7. Pay Annually (If You Can)

Paying for car insurance on a monthly direct debit is not a simple subscription; it is actually a high-interest loan. Insurers charge an Annual Percentage Rate (APR) to split the payments, which can add anywhere from 10% to 30% to the total cost. Paying the lump sum upfront is always the cheapest route.

Frequently Asked Questions (FAQ)

Is Third-Party insurance cheaper for young drivers?

Logically, you would think buying the lowest level of cover would be the cheapest. In reality, it is often the most expensive. Insurers realized years ago that high-risk drivers were overwhelmingly choosing Third-Party cover. Always quote for Fully Comprehensive first—it is almost always cheaper and provides vastly better protection.

Does completing the Pass Plus scheme lower my insurance?

While some niche insurers still offer a small discount for holding a Pass Plus certificate, the majority of mainstream insurers no longer factor it into their pricing. A telematics (black box) policy will yield much greater financial savings.

What happens if a young driver gets penalty points?

Under the New Drivers Act, if you receive six or more penalty points within two years of passing your test, your license will be automatically revoked. You will have to apply for a provisional license and pass both the theory and practical tests again.